Evaluate the capacity for detailed industry-occupation linkage to capture variation in AI exposure across industries

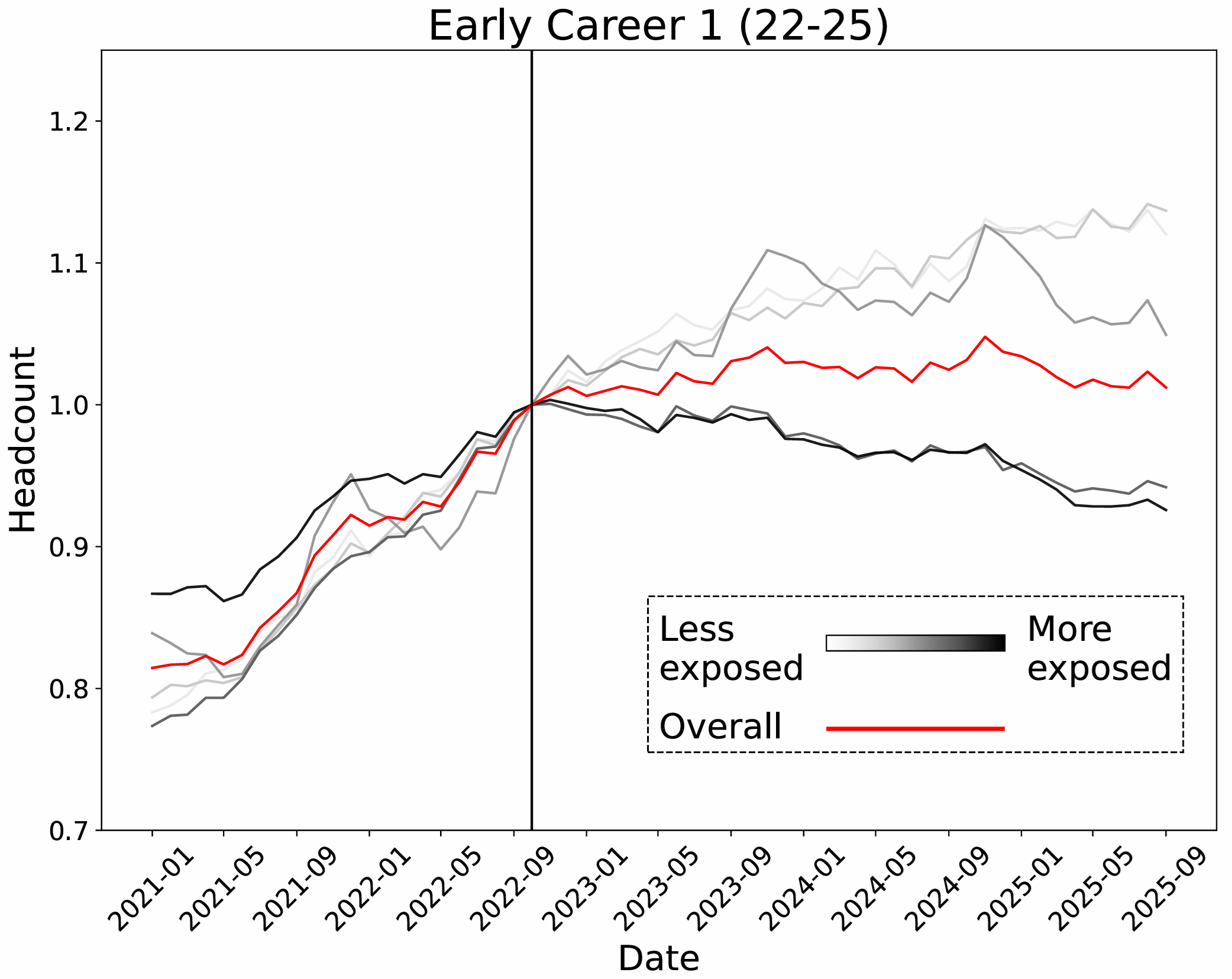

Replicate and extend recent results on early career workers using comprehensive administrative data

Investigate mechanisms using comprehensive information on hires, separations, and firm dynamics from the Quarterly Workforce Indicators (QWI)

Core findings

Employment/Earnings

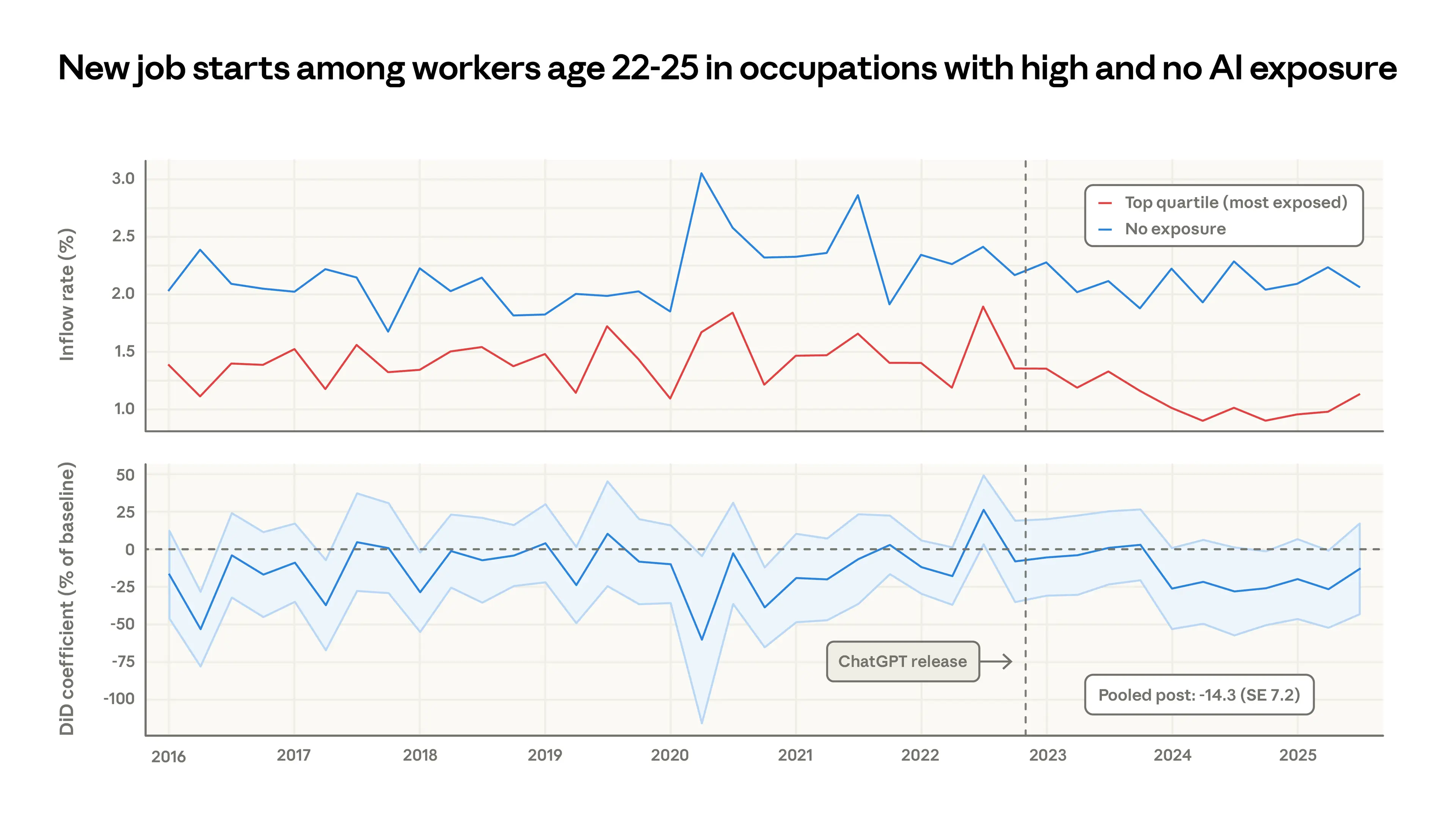

Employment of early career workers (ages 22-24) in the most AI-exposed industries declined 15% (-159k jobs) in the 10 quarters following the introduction of ChatGPT.

Declines in employment associated with AI exposure are broad-based across sectors.

Evidence on earnings is weaker, but suggestive of small relative earnings declines.

Mechanisms

Employment declines are driven by an immediate 9% decline in hires as well as compositional effects likely attributable to delayed hiring.

A decline in separations of early career workers in exposed industries partially offsets these mechanisms.

Additional findings

Timing and alternative explanations

Triple-difference analyses suggest that substitution away from early career workers may have begun with the COVID recession. Possible explanations include remote work and increased educational attainment.

Triple difference analyses of job gains/losses and backfill still show evidence of a discontinuity at ChatGPT’s release.

A local projections analysis shows that AI-exposed industries are historically not particularlty sensitive to monetary policy shocks. Such shocks might explain about 1/4 of the regression-adjusted gap in early career employment as of 2025q2, but don’t match the discontinuous drop in hires in exposed industries.

Primary data sources

Occupation AI exposure measure: Eloundou et al. (2023) GPT4 measure

ACS Public-use microdata: Crosswalk occupations to industry-states using 2015-2019 ACS 5-year estimates to obtain employment-weighted mean AI exposure

Quarterly Workforce Indicators (QWI): Published quarterly employment, earnings, hires, separations, and other measures at the 6-digit NAICS by state level, broken out into 8 age groups.

Data restrictions and notes:

QWI covers a near-universe of private sector employment by linking UI wage records to employment data from the Quarterly Census of Employment and Wages (QCEW)

I use data on all private employers in 45 states with data through 2025q2, excluding NAICS 92 (Public Administration)

QWI censors small cells (~1% of early career employment and hires)

QWI imputes workers to establishments, which can impact industry assignment in multi-establishment firms

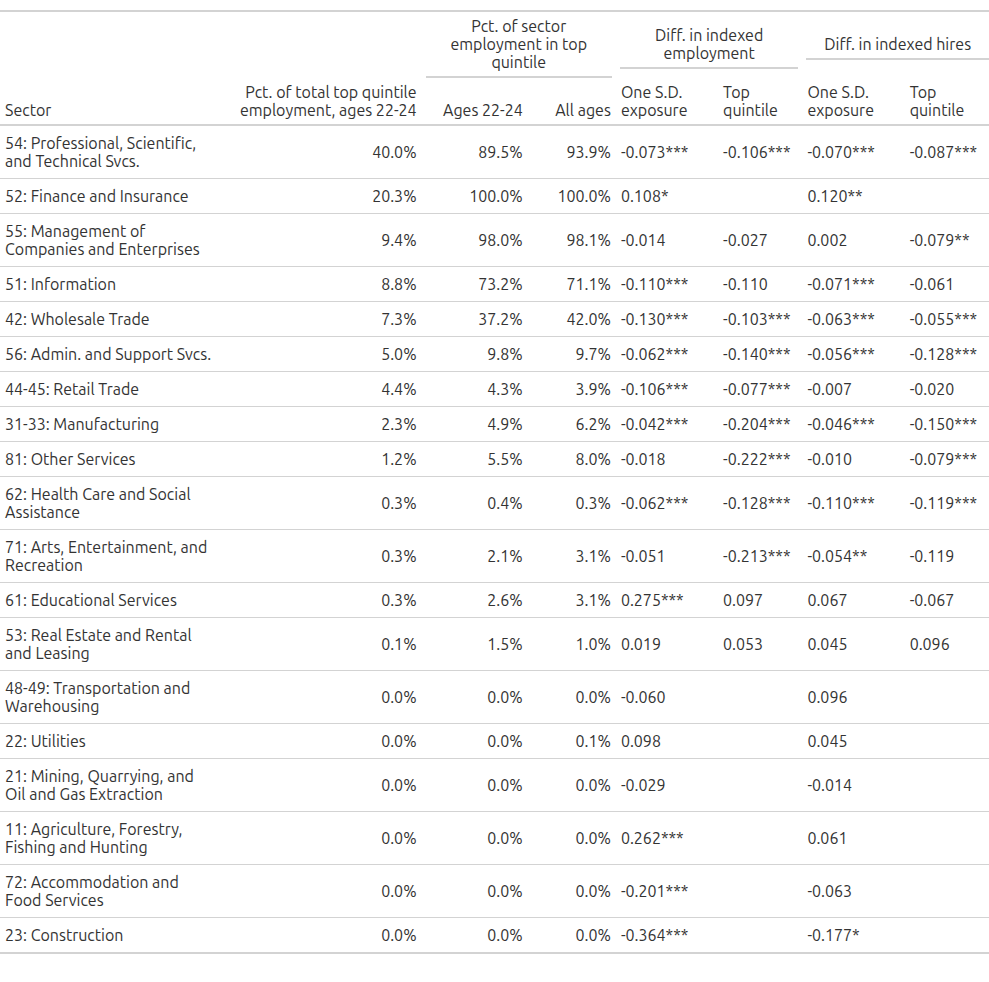

The top quintile of AI exposure is most concentrated in four sectors

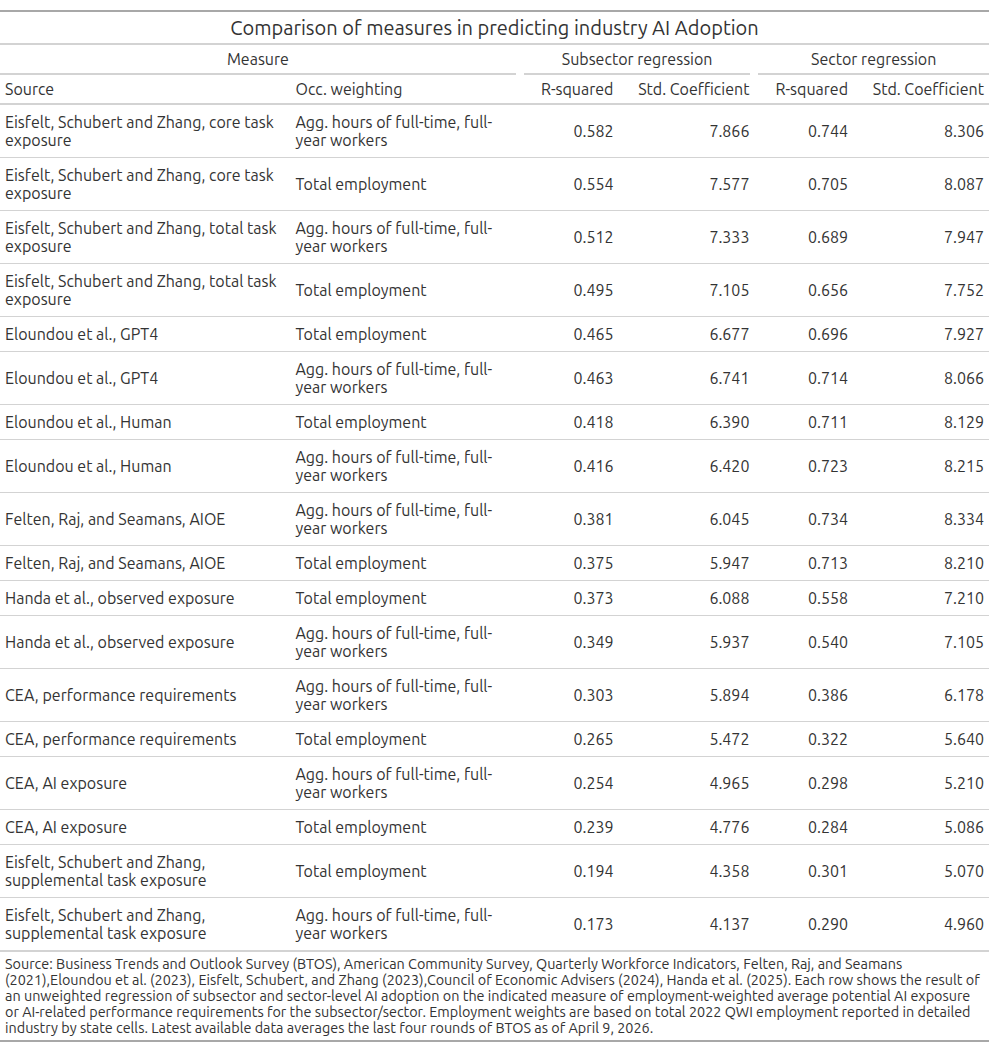

Crosswalked AI exposure is reasonably predictive of industry AI adoption

Early career employment in the most exposed quintile has declined 15% since 2022q4

Older age groups have not seen similar declines

Declines in early career employment are broad-based within the most exposed sectors

Regression specification

To formally test for changes in top-quintile outcomes, I run event study regressions of the form:

\(y_{i,s,t}\): logs of beginning-of-quarter employment, four quarter change in avg. monthly earnings for full-quarter workers, end-of-quarter hires, beginning-of-quarter separations, job growth, job loss, job replacement

\(\alpha_{i,s}\) and \(\gamma_{t}\): fixed effects for industry-state and time

\(\beta_{t}\): The estimated difference in outcome for the most exposed industry-states, net of time-invariant characteristics.

Regression samples are age-group specific (mostly 22-24). Reference period is 2022q4 for beginning-of-quarter measures (employment) and 2022q3 for end-of-quarter measures (hires, stable earnings, job growth/loss/replacement).

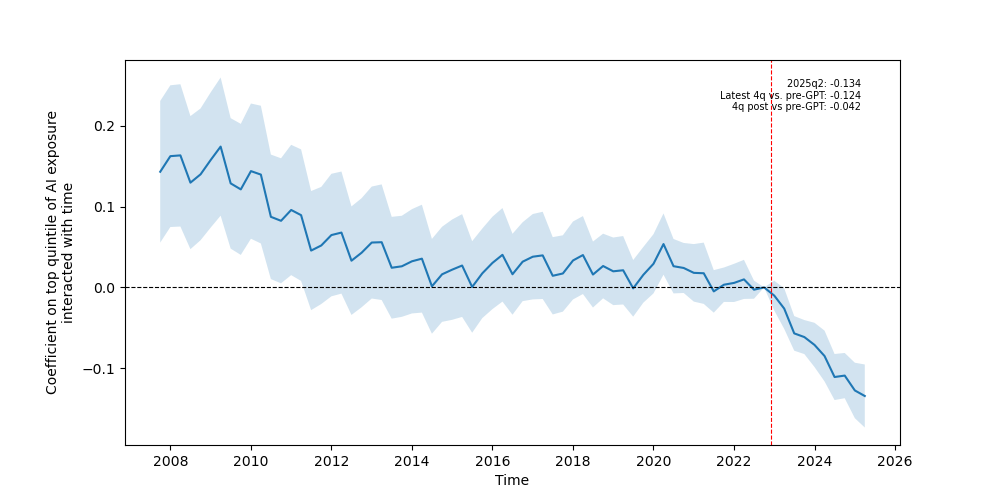

Event study: Employment of early career workers in the most exposed quintile (ages 22-24)

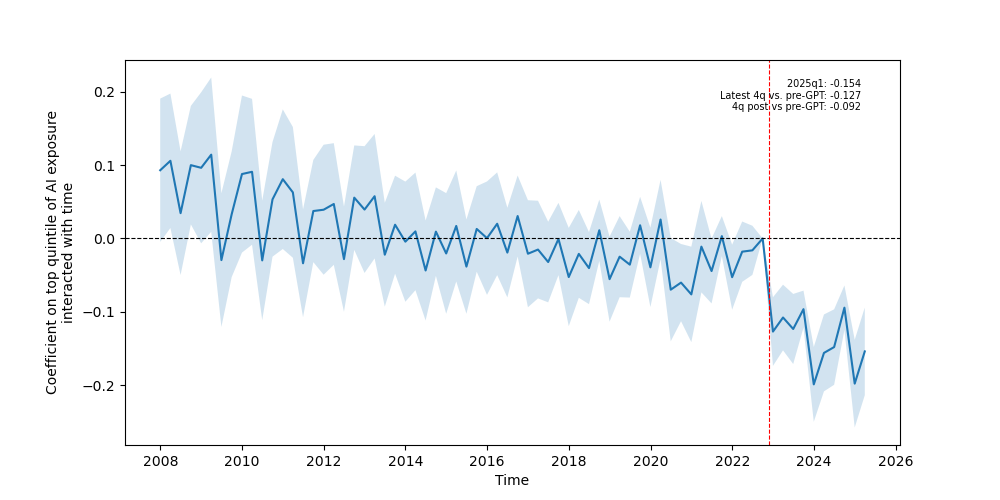

Event study: Hires of early career workers in the most exposed quintile

Event study: Separations of early career workers in the most exposed quintile

Counterfactual analysis shows the entire decline in early career employment is attributable to reduced hiring

Changes in employment within an age group are a function of net job flows plus composition effects (net age flows, NAICS changes, and imputations).

So, we can use the event study regression estimates on hires and separations to identify the contribution of each component to the counterfactual employment path.

Event study: YoY change in avg. monthly earnings of early career workers in the most exposed quintile

Triple difference regression specification

Employment and earnings changes over time are generally positivity correlated across age groups. We can look at how this relationship is changing in the top quintile using specifications of the form:

Here, the outcome for age group \(g\) is compared to the same covariate or another indicator for a different (older) age group.

The covariates of interest \(\delta_{t}\) estimates the extent to which the relationship between the two age groups is changing differently over time in the most exposed quintile.

Triple difference regressions show evidence of earlier declines

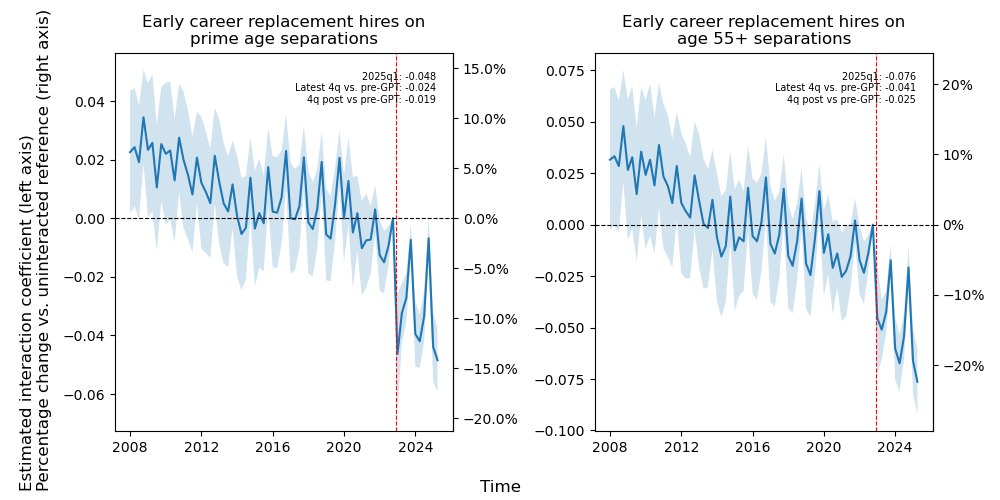

Growing AI-exposed firms became less likely to fill new positions with early career workers

Firms appear less likely to backfill separations with early career replacement hires

Crosswalking to industry allows us to test this hypothesis more formally by evaluating how AI exposure aligns with industries’ monetary policy sensitivity

Regression specification

I develop a local projections model (Jordà 2005) to estimate the sensitivity of each NAICS industry (4-digit) to unexpected monetary policy shocks using regressions of the form:

\(\beta_{i,h}\): Estimated sensitivity of industry \(i\) to shocks \(h\) periods later

All estimations are performed on \(t \le 2016q4\) so that all impulse response data excludes the COVID pandemic.

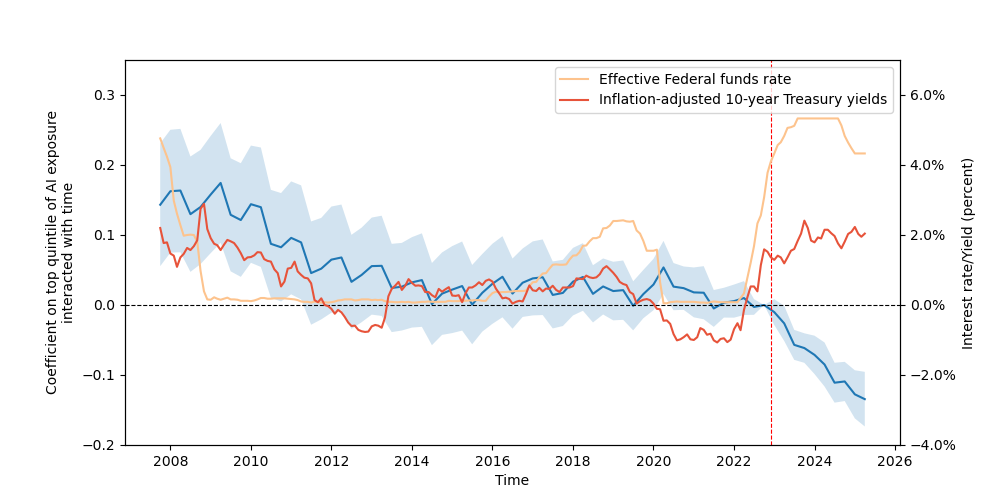

Monetary policy shocks do not disproportionately affect the most AI-exposed sectors except in early career employment

The cumulative effect of monetary policy shocks through 2023 may explain part of the early career employment gap, but it does not predict a gap in hires

Conclusions

Linking occupational AI exposure to industries is worth the tradeoffs

The rapid decline in hires following introduction of ChatGPT is consistent with a decline in relative demand for early career workers in AI-exposed industries

Regression analyses of employment and hiring changes are generally supportive of a discontinuity at ChatGPT adoption, but triple difference analysis suggests that changes in relative demand may have begun several years beforehand.

Historical monetary policy sensitivity appears to explain only a fraction of observed patterns

Further understanding of mechanisms will likely require linking sources of microdata on business AI adoption, worker occupation, and educational attainment

Appendix

Crosswalking from occupation to industry involves considerable loss of variation, but detailed industries help

Aggregation

Weighted parameters

Incremental information loss

Mean

Variance

MSE

ICC

Original ACS data

0.3419

0.0447

ACS occupation to industry-state

0.3419

0.0148

0.0299

0.3307

QWI 6-digit NAICS-state

0.3482

0.0150

6-digit NAICS-state to 6-digit NAICS

0.3482

0.0146

0.0004

0.9723

6-digit NAICS to 5-digit NAICS

0.3482

0.0146

0.0000

0.9991

5-digit NAICS to 4-digit NAICS

0.3482

0.0145

0.0001

0.9925

4-digit NAICS to 3-digit NAICS

0.3482

0.0118

0.0026

0.8174

3-digit NAICS to 2-digit NAICS

0.3482

0.0102

0.0016

0.8655

Validation: BTOS AI adoption on AI exposure measures

The association of AI exposure to early career employment declines is observed within most sectors

Event study: Job gains, job losses, and replacement hires of early career workers in the most exposed quintile

Composition effects suggest that age at labor market entry may be rising in AI-exposed industries

QWI contains two closely related measures of employment that arise from how quarterly earnings data are mapped to employment spells:

\(Emp_{i,s,g,t}\): Beginning-of-quarter employment in \(t\)

\(EmpEnd_{i,s,g,t-1}\): End-of-quarter employment in \(t-1\)

Within industries and age group tabulations, these differ because of:

Changes in establishment NAICS codes

Time-variant imputations

Younger workers aging into \(g\)

Older workers aging out of \(g\)

Since the first two effects are generally small and likely mean 0, we can effectively infer the net effect of aging from the ratio of \(Emp_{i,s,g,t}\) to \(EmpEnd_{i,s,g,t-1}\).

The slight decrease in this series over time is the source of composition effects in the counterfactual analysis. More precise analysis of entry patterns within the age bin will require restricted-use microdata.

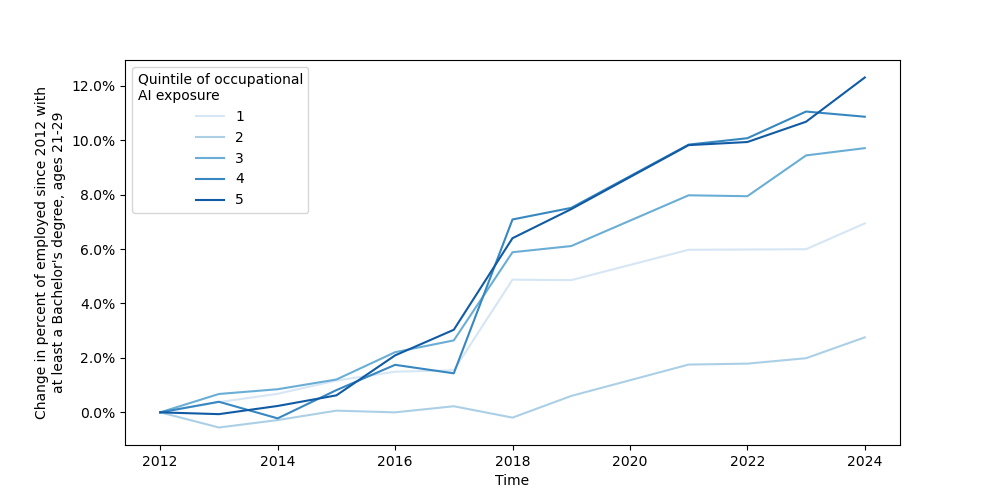

What is the contribution of increasing educational attainment?

Educational attainment of young workers has increased most in the highest quintile of occupational AI exposure. This could be a source of delayed labor market entry.

A decision to delay entry into the labor market has offsetting effects on employment dynamics at different times:

\(\Downarrow\) hires and employment (immediate)

\(\Uparrow\) hires (at future entry) or compositional adjustment (at time of age out)

Future work linking college graduates to their employment outcomes using PSEO may help identify and distinguish effects of delayed entry vs. slower job-finding after graduation among the most AI-exposed graduates.